New Federal Plan Will Cost New York Homebuyers More Money

The process to buy a home has a lot of steps and is often pretty complicated. With all of the laws that need to be followed and different things that come with the home shopping and closing process, it's often amazing that people are able to actually buy and sell houses, especially in a state like New York which makes it sort of complicated.

However, it's not all gloom and doom when buying a house, there is plenty of programs that exist to help people figure out the home-buying process, especially for first-time homebuyers. There are even a few financial assistance programs to help with additional cash if you come up short. This can be especially helpful in New York State because we have so many fees and taxes that get added to our mortgage loans.

But thanks to a new proposal from the Federal Government, it may start to cost us all a little more money to buy a house due to new interest fees that will be charged on mortgage loans.

Is The Federal Government Raising Mortgage Interest Rates?

According to a report from Newsweek, the Biden Administration is pushing the Federal Housing Finance Agency to adjust the way mortgage companies price their mortgage loan interest rates.

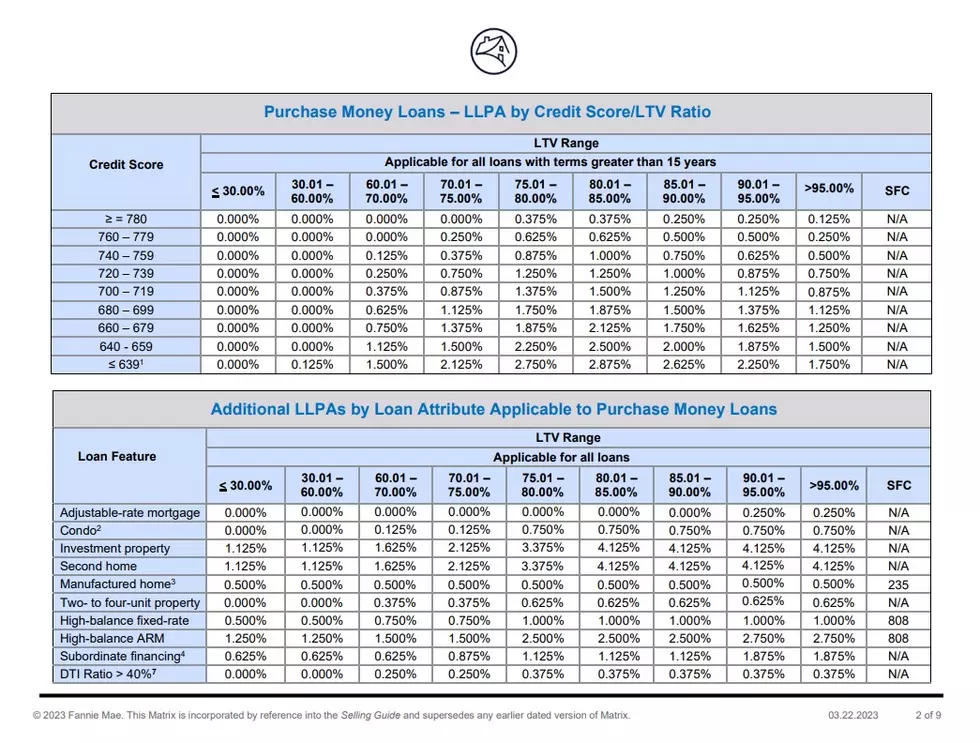

Each mortgage company and mortgage financier uses a pricing structure called a Loan-Level Price Adjustment Matrix. This is the planning document each mortgage company uses to determine how much additional interest someone would have to pay when being approved for a mortgage.

Under the new Biden plan, potential homebuyers who have good credit will begin to pay a higher interest rate. Those additional fees that are paid via the higher rates paid by borrowers with good credit will be used to reduce the cost of loans for borrowers who are struggling with their credit.

While this is good news for people with lower credit scores, it's going to make homebuying less affordable for those with better scores.

How Do These Mortgage Rate Changes Impact New Yorkers?

A recent review of national credit scores shows that, on average, New Yorkers have family good credit. While there are some pockets of the state that has below-average FICO scores, there are several communities that are doing quite well.

Since these rate increases will only impact those with better credit, it's going to hit New York more than other places.

Unique Triangle House In Buffalo For Sale

Gallery Credit: Ed Nice

5 Things New York Should Ban But Never Will

Gallery Credit: Ed Nice

More From 93.7 WBLK